Investing can feel like navigating a winding mountain path: the higher you climb, the broader the view—but the steeper the rock face. Understanding where assets sit on the spectrum between safety and growth empowers you to chart a route that aligns with your dreams and tolerance for uncertainty.

At its heart, the risk-reward spectrum visualizes the inverse relationship between potential return and exposure to uncertainty. Simply put, taking on more volatility can open the door to greater profits, but it also widens the range of possible outcomes.

Expected return is the weighted average of all possible outcomes, and as risk rises, that distribution fans out—amplifying both upside and downside possibilities. No investment is free from danger; even cash can lose purchasing power when inflation outpaces interest.

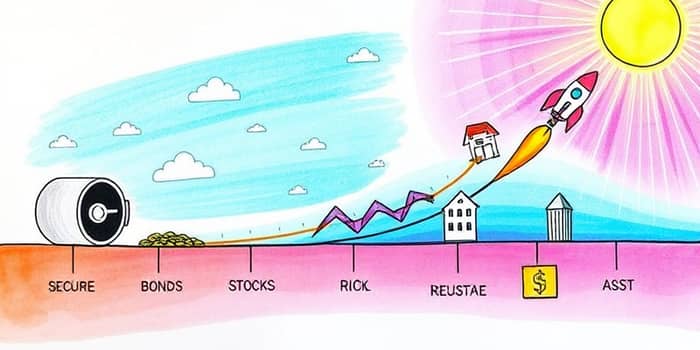

Assets from cash to cutting-edge alternatives occupy positions that reflect how much stability or growth potential they offer. By understanding these categories, you can assemble a diversified portfolio tailored to your horizon and goals.

For instance, a 50/50 blend of stocks and bonds can halve the impact of a market crash, yet also temper the thrill of a bull run. Moving further along the spectrum—from balanced funds to small-cap or sector-specific equities—pushes both risk and reward higher.

Risk is not monolithic. Different threats can eat away at returns unless actively measured and managed.

Risk-adjusted metrics—such as the Sharpe Ratio, Sortino Ratio, or Treynor Ratio—help compare how much return you earn per unit of volatility or downside exposure.

Balancing the spectrum isn’t guesswork. Investors use a toolkit of techniques to pursue gains while protecting capital.

Most professionals combine diversification, hedging, dynamic monitoring, and disciplined rebalancing within integrated platforms. This coherent approach helps you anticipate stress-test scenarios—such as rising rates or economic downturns—while staying aligned with long-term goals.

Your unique financial journey hinges on four pillars: risk tolerance (how much volatility you can stomach), risk capacity (how much loss you can afford), time horizon (years until you need the money), and financial goals (growth, income, preservation).

Start by mapping these dimensions, then select asset classes that fit. A younger investor facing decades until retirement might tilt heavily toward equities and alternatives, harnessing compounding returns and recovery potential. Someone nearing a major purchase may favor cash and high-quality bonds to protect principal.

Real-world examples drive the lesson home: an investor who allocated a house down-payment fund to equities faced a three-year drawdown and was forced to sell at a loss. In contrast, those who kept that money in stable fixed income avoided emotional panic and preserved their buying power.

No plan is set in stone. Markets evolve, personal situations change, and new opportunities arise. Adopt a four-step cycle:

Always remember: no strategy eliminates risk entirely, but a well-constructed framework can manage uncertainties and capture growth.

Investing is a journey, not a destination. By mastering the risk-reward spectrum and applying thoughtful strategies, you gain confidence to navigate storms and climb toward rewarding peaks. Patient discipline, continuous learning, and periodic check-ups will keep your portfolio healthy through every market cycle.

Ultimately, success lies in aligning your investments with your deepest aspirations—combining diversification plus disciplined approach to build wealth that supports your life’s purpose.

References